How to turn £2,400 into £20,000 with simple financial magic

And without taking any silly investment risks

How would you like to learn some real financial magic?

Well, this might be one of the most magical money ideas you’ll ever see.

But, before you read on, I must warn you . . . the key idea here might not help you personally. It all depends on your circumstances.

That said, if you share it and it helps one of your friends, I think they’ll love you for it.

Now there are a few ideas in this post – but the headline idea will only work for people with ‘wealthy’ parents OR . . .

. . . other, super generous, wealthy relatives or friends.

But either way, what I hope you’ll see here (and elsewhere on this site) is that proper financial planning is one of * the secrets to acquiring (and keeping) wealth over the long term.

it certainly beats messing about in speculative games – in Bitcoin or any other ‘hot’ investment !

The madly powerful idea below is just a small part of a much chunkier Insight into the key areas of sound financial life planning.

Areas we all need to address – wealthy or not. So, be sure to grab the ideas from that one too

If the big idea below doesn’t help you today, I promise you that those other ideas will give you a solid financial framework for your future.

What’s more, if one day you are the wealthy parent we talk about below – you will definitely want to remember this idea.

*BTW – the other secrets include having great sales and marketing and relationship building skills, a serious work ethic and an obsession with the delivery of quality work to your customers . . . or your boss 😉

And, if you need help on the sales and marketing front – I might very well be able to help you there too.

Either way, stay tuned for ideas via my Newsletter or Facebook Group – see bottom of page for links.

Now, to lead us into the ‘financial magic’ . . .

try these ‘top tips’ on money and life

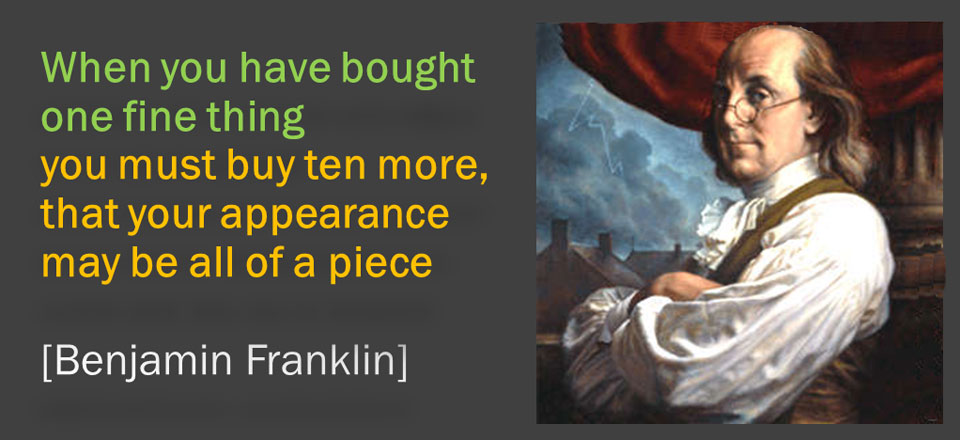

From Benjamin Franklin

And in case you’re not sure who Franklin was . . .

He was an intellectual powerhouse, a leading US politician, an author, a printer, a satirist, a political theorist, a scientist and an inventor.

So, he kept himself busy 🙂

He invented the Franklin stove, the carriage odometer, the lightning rod and bifocal glasses!

He was passionate about liberty (coupled with responsibility, thrift and hard work) and he formed the first public libraries in the USA.

He’s also credited with securing France’s help to the Americans in the War of Independence against the British . . .

. . . although you’ve got to question whether the French needed much persuasion about that !

In his book The Way to Wealth (1758), Franklin compressed 25 years’ worth of maxims from his best-selling annual publication Poor Richard’s Almanac.

And, his advice for financial magic – and a better way of life had two main themes:

- Industry (hard work and commitment to the cause) and

- Thrift (the careful management of time and money).

Interestingly, the benefits of thrift were promoted by Prime Minister David Cameron in the aftermath of the financial crisis in 2008-09.

And ‘thrift’ is certainly a more attractive word than ‘austerity’ to describe a plan to pay down debt.

In the heady, debt-fuelled consumer boom years up to 2007 we might have scoffed at Franklin’s ideas for a better way of life. But thrifty ideas were very modern thinking – at least a few years back.

Sadly debt has now taken off again and we’re almost certainly heading for another crisis as a result. But enough of the gloom:-)

Here are some of Franklin’s maxims which, I’m sure you’ll agree, are as relevant today as they were when he wrote them 260 years ago:

- Early to bed, and early to rise, makes a man healthy, wealthy and wise.

- Diligence is the mother of good luck.

- Little strokes fell great oaks.

- There are no gains, without pains.

- Dost thou love life? Then do not squander time, for that’s the stuff that life is made of.

- Beware of little expenses; a small leak will sink a great ship.

- When the well’s dry, they know the worth of water.

- What maintains one vice, would bring up two children.

- When you have bought one fine thing you must buy ten more, that your appearance maybe all of a piece. (Shopaholics and brand victims take note.)

- The borrower is a slave to the lender.

- Employ thy time well if thou meanest to gain leisure.

- The only certainties in life are death and taxes.

What wonderfully solid and simple advice about money and life.

That last quote is one of Franklin’s most famous – and is certainly borne out by history.

Did you know that income tax was first introduced as a temporary measure in the UK – in 1799?

So, for more than 200 years we’ve been suffering a temporary tax! And for 200 years before that, the government’s main source of revenue was through land tax, which many would argue should be reintroduced today – and there’s certainly an argument that they’re fairer than taxing the people who work to generate the wealth.

Franklin was wrong about UK death taxes

Apologies for that digression but you’ll soon see the link now.

This magical idea is all about saving death duties – or Inheritance tax (IHT) as we now call them here in the UK.

So, this is tax payable on the value of your estate (on your death) if the ‘taxable’ parts of it exceed a certain ‘tax free’ amount.

And the simple truth is that, for many people, despite Franklin’s assertion, it’s not ‘certain’ that you’ll get hit by this death tax . . .

. . . even if your estate is worth more than the tax free amount.

IHT is a “voluntary tax” and there are a lot of simple ways to escape it.

And no, I’m not talking about dodgy tax schemes here. I really would NOT recommend you get involved in that stuff. You can safely leave those games to Jimmy Carr and other celebrities.

One way to think about IHT is that the taxman simply wants you to move the money on – to give it away if you don’t need it – to where it might be spent and do some good in the economy (and generate other taxes of course 😉

So, even Roy Jenkins, the former Labour chancellor, said that inheritance tax was voluntary.

Here’s how he described it:

“Inheritance tax is a voluntary levy

paid by those who distrust their heirs

more than they dislike the Inland Revenue.”

Jenkins was a smart and witty politician. A type of which, sadly, we don’t have too many these days.

Today’s politicians are, as a good friend of mine once said, ‘rather too earnest in their mediocrity’ 🙂

The question for you, if you have wealthy parents, is how to reduce the impact of IHT on their estate – assuming they’d like to.

Will their current arrangements ensure that their assets are left to the people or organisations they wish to benefit?

And, in the shares that they want them to have?

Do you know if and by how much their estate will be hit by Inheritance tax after they’ve gone?

Did you know that it’s quite common

for the taxman to end up taking more from an estate

than is left to any other beneficiary!

Would they (and you) be happy with that?

So, let’s do this financial magic

And turn £2,400 into £20,000 – without taking silly investment risks

Okay, so I’m going to assume that you are a young (ish) person (by that I mean someone between 25 and 50!) with wealthy parents . . .

. . . but that you’re ‘some way off’ being on track with your own personal retirement income plans.

If you’re the parent reading this – it should still make perfect sense. You might think that there’s not much in this idea for you but I’d disagree.

I think the benefits are enormous in terms of improved goodwill in the family – with such arrangements.

Of course you should only consider ideas like this if they’re suitable to your personal circumstances. And to know that – you’d need to take competent and qualified guidance.

Now back to the story!

So, how about asking (or getting someone else to ask!) your parents to fund your pension for you?

Are they wealthy enough to afford it?

Are they going to leave you a lot of money in their will anyway?

If so then, absent any other tax mitigation strategies, here’s the NEWS.

YOU are going to lose 40% of your inheritance – at the margin.

What?

Oh, yes, that number surprises most people.

And it’s especially shocking when you think that a lot of people’s wealth is built up from income that’s already taxed when earned . . .

. . . and, unless it’s all stored in tax free ISAs – has been taxed again within bank accounts and investments.

But that’s the simple truth of it – whether the money sits in ISAs or not . . .

. . . if your parents ‘taxable’ estate exceeds the ‘IHT nil rate band’ (and we won’t cover all the grisly details here) then

40% of the excess will be taken by the taxman when they’re gone.

However . . .

. . . if they decided to pass some money to you today (or sometime soon) then those gifts might* very well escape all of that IHT 🙂

*The rules and allowances are too complicated to summarize in this short post – but that’s the principle of it.

Wow!

Yes, wow . . . but this is not new.

Like I (and Roy Jenkins) said a long time ago, this tax is voluntary.

And this ideas gets better too.

Let’s look at a quick example

Let’s say that your parents gave you £4,000 today and you agreed to put it in your pension.

I suspect that this would please most parents – because they’d then know that you couldn’t spend it today.

The rules on pensions are (generally) that your money is tied up until 10 years before state retirement age.

Of course, if your parents are funding your pension, that might mean that you can relax a bit . . .

. . . and allow yourself to spend it bit more on the things you need today too 🙂

Anyway, you pop the £4,000 into your pension (or your parent puts it in for you – but that’s another story) . . .

. . . and then even more magic happens.

That £4,000 is immediately turned into £5,000 – because of the 25% boost from basic rate income tax relief.

(and, if you’re a higher rate taxpayer, you’d enjoy a tax refund also!)

And, that £5,000 might then become £10,000 – almost immediately, if you’re getting matched payments on your pension from your employer.

And it could easily turn into £20,000, in today’s money terms (assuming very modest investment growth) over the next 15 to 20 years whilst your parents are, hopefully, still around.

But what would happen if your parents simply held onto the money?

And they kept it in a nice safe bank deposit account for you – until they’re gone then . . .

Well, in that case, you’d likely only receive £2,400 (in today’s money terms ) from what could otherwise have been a £4,000 gift.

What?

Yes, well, £4,000 sat in a bank account over 10 or 20 years is unlikely to grow any faster than inflation.

So, it’ll probably still be worth just £4,000 in future years – or possibly a bit less.

And then, after the tax man has taken his 40% IHT – you’d receive £2,400!

So, between you and your parents, I’d seriously encourage you to . . .

work out whether you want £20,000 or £2,400!

It’s a bit of a no brainer really eh?

And when you factor in the possibility of Jezza Corbyn taking control of our government . . .

. . . I’m not sure that ‘waiting and accepting’ a 40% IHT tax hit is a great idea.

After all, he could come in and crank up those rates very quickly.

So, if IHT is an issue for your family – and your parents can afford to do something about it – they might want to think about using the windows of opportunity to save some of it – sooner rather than later.

Okay, so, if you didn’t before, now you know that there can be some BIG benefits to sensible ‘financial planning’

But please remember two things about long term, personal financial life planning . . .

Number 1 – it’s ‘long term’

And 2 – it’s ‘personal’ 😉

The single idea we’ve explored here is NOT advice.

It’s just one example of many ideas that can work for some families in some circumstances.

You need to take a strategic approach to planning your personal finances. And, if you’ve not explored financial planning before, you need a framework for approaching it.

You can find one of those right here.

And, if you’d like my help with personal or group education on financial planning, pension planning and investing – then just contact me from here.

The good news is that you can about this stuff – without telling me anything about your personal finances.

And that’s how I operate my group workshops . . . lot’s of fun and ideas – but no one says anything about their personal situation.

Education is just that – it’s a one way transfer of knowledge and skills. So, if just want some lessons on the fundamentals of personal finance – that’s okay by me.

Education is just that – it’s a one way transfer of knowledge and skills. So, if just want some lessons on the fundamentals of personal finance – that’s okay by me.

On the other hand, if you’d like me to help you understand your personal finances in detail, that’s fine too. This would be a private coaching engagement . . .

. . . but we can do the education alongside if you like.

Just let me know the sort of help you want.

And, in the meantime, be sure to join my Wealth-builders Facebook Group – or sign up to my newsletters.

That way you can get all these ideas – for planning your money and making more of it – as soon as I publish them.

All the best for now

To share your comments below – log in with your social media or DISQUS account

OR, to “post as a guest” , just add your name and that option will pop up.

To learn about other thinkers / books I RATE, click here

Or for regular ideas – for achieving more

Join my Facebook group here

Or, for occasional updates by newsletter

And free downloads including: My ‘5 IRATE Steps for planning your Financial Freedom’

and the first chapter of my book, ‘Who misleads you about money?’ click this image

Discuss this article