Get your teenagers flying

teach them to invest *early* in themselves

On this site, and in my book, ‘Who can you trust about money?’ I focus on ideas to help you achieve more of what matters to you – for yourself or your loved ones.

Here I want to share one simple but powerful idea (with many applications in life) which could help any teenager make more of their greatest asset (themselves)

How to build funds for their education

Now, before we get into the lesson for your teenager… let’s quickly look at how the same idea (of starting early) can help us with our long term savings.

Here we see the pain of having to pay, at the last minute, out of income to help a child through College or University (the red bars) versus taking the easier long term savings route (in blue)

Note: The amounts shown are all in today’s money terms.

Note: The amounts shown are all in today’s money terms.

Of course, it doesn’t matter whether we’re saving long term for a University Support fund or a pension… or saving over a shorter term for a deposit on a house, a new car, computer, holiday, or whatever…

… We’ll often have the same choice when it comes to funding our big financial life goals.

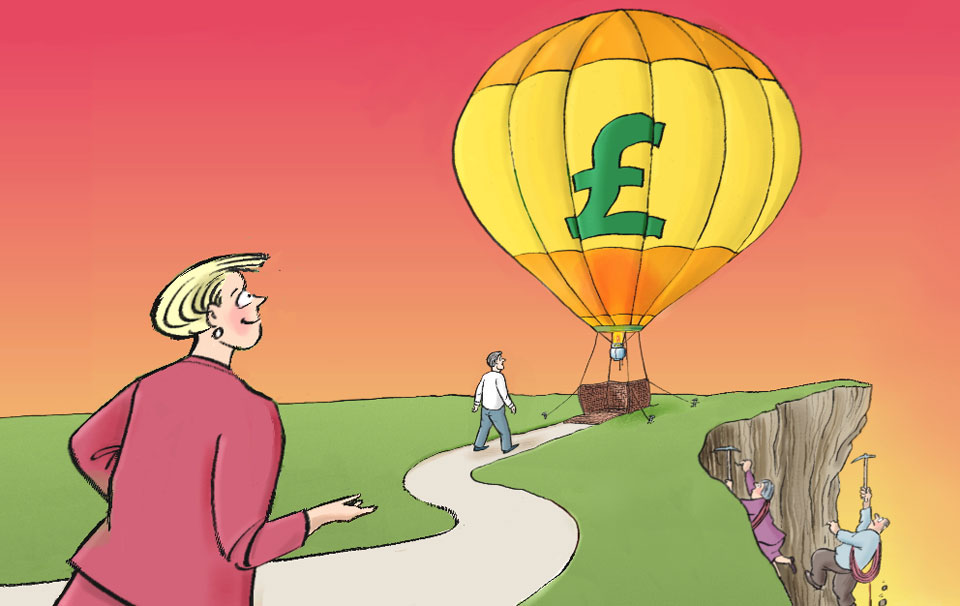

We can either take the easy, gentle road – and save up for this stuff. Or, have a last minute panic to reach our goal – that will often mean taking on more debt.

So, logically there’s no contest

So, logically there’s no contest

None of us would choose to make that impossible climb up a financial cliff face at the last minute… when we could easily have built up the funds we needed by saving a little each month.

Sadly, we humans don’t act logically a lot of the time. So, we often end up leaving it too late to save… and then waste vast sums paying debt interest.

Of course, some borrowing can be helpful some of the time – to smooth out the cash flow. Some debt might be OK, if what you buy with it yields a higher return than your borrowing costs.

Taking out a student loan to pay fees for higher education… or a personal loan to buy a car to get to work, are two such examples.

The goal you can’t fund with borrowed money

That said, it’s worth remembering that one of our biggest financial life goals cannot be bought with borrowed money.

Unless we have another plan for income in our later years, we simply must save towards a pension. The good news is that with 30+ years of time to do this, it doesn’t have to be that painful.

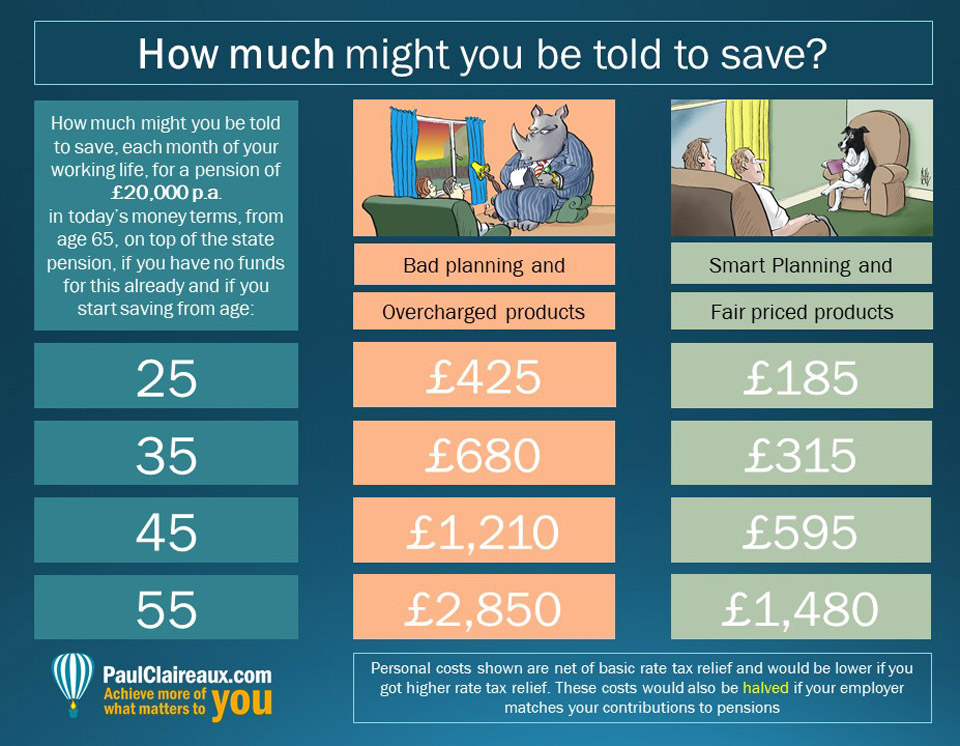

‘Time’ really is your friend – when it comes to long term saving, as we can see here in a table that shows both the benefits of early and wise saving choices.

Remember you’re different to others

There is, of course, more to this than simply saving enough.

We need to know how to invest wisely for the long term which includes knowing how to choose the right (low cost) financial products for our personal situation.

And it’s essential to understand that we’re each unique in ways that matter to planning our finances

Helping younger folk to ‘get’ this early

Now, we know that younger people heading towards University or College have lots of other financial challenges to deal with… and the last thing they’ll want to think about is their pension! 😉

However, this ‘wall of pain’ concept can help them with their studies too… and, if they grasp this ‘investing early’ idea at a young age, there’s a much better chance that they’ll get on with their savings too, when they need to.

Treat study as an investment in self

We also know that studies, like any personal goal, can become impossible to complete, if we ‘mess about’ (for too long) before getting started.

Everyone but the model student feels the pain of procrastination as exam season approaches.

You remember those times, right?

So, how can you motivate your teenagers to want to get on top of their work at the start of each academic year?

Well, here’s one conversation you could try.

The delaying studies riddle

This is a very rough script of the sort of question you could ask your teenager,

I want you to imagine you’ve started at college / University…

… you have a lot of fun in Freshers week…

… you take another week to recover from that… and you really don’t get on top of your work in the first term… because you know you’ve got two more terms to catch up.

Now, imagine that in your first term, your ‘fecking about’ (staying out half the night, getting up late, wasting hours on Facebook or computer games and missing lectures) means… that you complete just one-third of the work you need to – to have a fair chance of getting good marks by the end of the year.

How much harder will you then have to work for the next two terms – to catch up?

Now, you might want to let your teenager, think about that question for a while… and let them have a guess at the answer… before you reveal it.

Answering our own, difficult, questions is, after all, how we ‘buy in’ to the need to solve them.

The chances are, unless your teenager is a Maths whizz, that they’ll guess they’ll need to work about twice as hard in terms two and three than they did in term one.

Here’s the real answer!

The answer, as you may have worked out… is that they’ll need to work four times as hard … and consistently so – for terms two and three, just to catch up.

Here’s the proof, it’s quite simple.

- In term one, they complete 1/3 of one term’s work.

- So, that’s 1/9 of a year’s work.

- Leaving them with 8/9 of the year’s work to complete over the following two terms.

- So, that’s 4/9 in each of those terms.

And 4/9 is, of course, four times the 1/9 they completed in the first term.

Oh, and if they decided that they needed to ‘catch up’ in term 2, to have a normal (relatively stress-free) final term… well, the term 2 catch up work rate will be five times that of term 1.

The picture proof is here

My experience

Now I wish someone had explained these facts to me before I ‘drifted’ into University to start an Honours degree course, in combined Electrical and Electronic Engineering in 1978 … because that didn’t work out so well 🙁

I was pretty good at Maths and managed to get through the first year but then the ‘backlog’ caught up with me and the whole thing went pear-shaped!

My challenge was arguably made worse by the fact that I was sent off to school a year early… finding myself at secondary school at age 10 and at the Student Union bar at University at 17!

In theory too young to drink a beer, but that didn’t stop me of course 😉

So, I’d certainly recommend a maturity-developing gap year, if it’s possible, for any teenager before heading into higher education.

Especially if their course is an intense one, in any of the STEM (Science, Technology, Engineering and Maths) subjects because our simple four times work rate catch-up formula won’t work on those courses anyway.

A lot of the study modules in STEM subjects assume knowledge of the earlier ones. So, these courses are like a chain… break a link and you break the chain… and you’re somewhat ‘stuffed’ if you don’t keep up – as I found to my cost!

Talk to your teenagers early

Okay, so I hope this is a useful idea… and I guess the question is what you might do with it?

If you have a teenager who needs a ‘nudge’ towards a more consistent working pattern…you could just send them a link to this Insight.

Or, you could go for the conversation and question approach, without simply giving them the answer. Which is, without question, the most powerful way to tackle this.

This fundamental truth – about the value of investing early – is certainly one worth sharing with your teenagers. But I’m under no illusion that this ‘wall of pain’ logic, on its own, will motivate a student to work harder.

Logical arguments, on their own, often fail.

However, if blended with other messages around the long-term benefits of steady work, this ‘procrastination pain’ message can be very effective…

… and, if you discuss this before the start of a year (and make your intentions clear, that you want to help them avoid unnecessary stress), then it could be a real game changer.

Whatever approach you take, I wish you good luck with this – and on every front – with your children.

I know it’s not always easy… and they don’t always thank you for everything you do.

… but hey, if they did that, how would you get a sense of achievement from your parenting? 😉

All the best for now and thanks for dropping in,

Paul

For more ideas to make more of your money and earn more of it too … Join my Facebook Group or sign up to my Newsletter and…

as a thank you, I’ll send you my ‘5 Steps for planning your Financial Freedom’ … and the first chapter of my book, ‘Who misleads you about money?’

If you’d like more frequent ideas (and more interaction) …join my facebook group here

If you’d like more frequent ideas (and more interaction) …join my facebook group here

And feel free to share your thoughts in the comments below

You can comment as a guest (just tick that box) or log in with your social media or DISQUS account.

Discuss this article